Between 1980 and 2024, Alabama was affected by 116 weather and climate disasters that each exceeded $1 billion in losses, according to NOAA’s National Centers for Environmental Information. These included 58 severe storm events, 26 tropical cyclones, and 2 major flooding events. In the most recent five-year period alone, Alabama averaged 6.4 billion-dollar weather events per year. Yet after the storms pass, thousands of Alabamians face a second disaster: insurance companies that deny, delay, or drastically underpay their property damage claims. This guide explains your legal rights after a natural disaster in Alabama — and what you can do when your insurer refuses to honor its commitments.

Why Alabama Faces More Disaster Risk Than Almost Any Other State

Alabama sits at the intersection of nearly every major natural disaster category. The state averages over 40 confirmed tornadoes per year, according to the NWS Birmingham tornado database, which has documented 3,444 tornado events in Alabama since 1680. Mobile, Jefferson, and Baldwin counties alone account for 11% of all tornado activity statewide.

Alabama also lies directly in the path of Gulf Coast hurricanes and tropical storms. NOAA data shows 26 tropical cyclone events have caused billion-dollar-plus damage in Alabama since 1980. In September 2024, Hurricane Helene triggered a Presidential emergency declaration (FEMA-3618-EM) for Houston County, Alabama.

The state receives an average of 56 inches of rainfall annually, making flood damage a persistent concern. And critically, standard homeowners insurance policies in Alabama do not cover flood damage — a gap that catches many homeowners off guard after major storms.

The April 27, 2011 Super Outbreak remains the defining disaster in Alabama’s modern history. That single day produced 62 confirmed tornadoes across the state, including 8 rated EF-4 and 3 rated EF-5. According to a peer-reviewed study published in the American Journal of Public Health, the outbreak caused 247 fatalities, over 2,000 injuries, and $4.2 billion in property damage in Alabama alone. The Tuscaloosa-Birmingham EF-4 tornado carved an 80-mile path, destroyed 12% of the city of Tuscaloosa, and generated $2.4 billion in damage — making it the costliest single tornado in U.S. history at the time. FEMA reported that more than 23,000 homes were damaged or destroyed statewide.

It was in the aftermath of that 2011 outbreak that the attorneys at Strickland Law Group formed a separate disaster claims practice to represent businesses and individuals whose insurance companies were underpaying storm damage claims. That practice has continued ever since, covering tornadoes, hurricanes, earthquakes, fires, and other natural disasters across the United States.

What Your Alabama Homeowners Insurance Actually Covers After a Storm

2")

Understanding what your policy covers — and what it excludes — is essential before you file any claim. Most standard Alabama homeowners insurance policies cover the following disaster-related damages:

- Wind damage from tornadoes, hurricanes, and severe thunderstorms

- Hail damage to roofing, siding, and exterior structures

- Lightning strikes that cause fire or electrical damage

- Falling objects including trees and debris

- Additional living expenses (ALE) for temporary housing if your home is uninhabitable

However, standard policies typically exclude:

- Flood damage — This requires a separate National Flood Insurance Program (NFIP) policy or a private flood insurance policy. Alabama communities that participate in the NFIP can access federal flood insurance, but many homeowners do not carry it.

- Earthquake damage — Requires a separate endorsement or standalone policy.

- Sewer and drain backup — Often excluded unless you purchase additional coverage.

- Gradual damage — Insurers often argue that storm damage was actually caused by long-term wear, poor maintenance, or pre-existing conditions.

This last exclusion — gradual damage versus storm damage — is one of the most common reasons insurers deny Alabama disaster claims. The Alabama Supreme Court addressed this precise dispute in State Farm Fire & Casualty Co. v. Brechbill (2013), where a homeowner’s claim for interior structural damage after a windstorm was denied because State Farm’s hired engineer attributed the damage to “wear and tear,” despite pre-storm inspections showing no structural issues.

How Insurance Companies Deny and Underpay Alabama Storm Claims

After major storms, insurance companies process thousands of claims simultaneously. Their financial incentive is to pay out as little as possible. Common tactics used against Alabama disaster claimants include:

Denying the claim outright. Insurers may claim the damage is excluded under your policy — for example, arguing that water damage came from flooding (not covered) rather than wind-driven rain (covered). After hurricanes, the distinction between wind damage and flood damage becomes a major battleground.

Underpaying the claim. Insurance adjusters may undervalue your property damage by using depreciated actual cash value instead of replacement cost, by failing to account for hidden structural damage, or by relying on lowball repair estimates from contractor networks that work with the insurance company.

Delaying the claim. Alabama Insurance Code Chapter 482-1-125 requires insurers to notify you of the acceptance or denial of your claim within 30 days after receiving proof of loss. But insurers frequently drag out investigations, request excessive documentation, or simply stop responding — banking on the fact that storm-devastated homeowners will accept whatever is offered just to begin rebuilding.

Blaming pre-existing conditions. This was the strategy in the Brechbill case. Insurers hire engineering firms to inspect damaged properties and attribute the damage to age, settling, or poor construction rather than the storm. This tactic is especially common with older homes.

Pressuring quick settlements. In the chaos following a major disaster, adjusters may arrive within days offering checks that cover only a fraction of the actual damage. Once you accept a settlement, it becomes much harder — though not impossible — to pursue additional compensation.

Alabama Bad Faith Insurance Law: Your Most Powerful Legal Tool

When an insurance company denies your valid storm claim without a legitimate reason, Alabama law gives you the right to sue for bad faith. This is one of the most powerful legal tools available to disaster victims, because a bad faith lawsuit can recover damages far beyond what the original insurance policy would have paid.

Alabama has recognized insurance bad faith as a personal injury tort since the Alabama Supreme Court’s 1981 decision in Gulf Atlantic Life Insurance Co. v. Barnes (405 So. 2d 916). Because bad faith is a tort — not just a contract dispute — successful plaintiffs can recover:

- Compensatory damages — The full amount owed under the policy, plus economic losses that resulted from the denial (such as increased repair costs during the delay, temporary housing expenses, and lost rental income).

- Mental anguish damages — The Alabama Supreme Court confirmed in Independent Fire Insurance Co. v. Lunsford (621 So. 2d 977, 1993) that mental anguish damages are recoverable in breach of homeowners insurance contracts, recognizing that a home is “so coupled with matters of mental solicitude” that a breach will “necessarily or reasonably result in mental anguish.”

- Punitive damages — Alabama law allows punitive damages up to three times the total compensatory damages, capped at $1.5 million, when the insurer acted with malice, fraud, or reckless disregard for the policyholder’s rights.

There are two types of bad faith claims in Alabama. A “normal” bad faith claim requires proving that the insurer had no legitimate reason to deny your claim. An “abnormal” bad faith claim — also called a failure-to-investigate claim — applies when the insurer intentionally failed to properly investigate before denying coverage.

The statute of limitations for filing a bad faith insurance lawsuit in Alabama is two years from the date of the insurer’s wrongful action, under Alabama Code § 6-2-38.

FEMA Disaster Assistance: What It Covers and What It Does Not

When a disaster is severe enough to trigger a Presidential declaration, FEMA disaster assistance becomes available to affected Alabama residents. However, FEMA assistance is often misunderstood. It is not a replacement for insurance.

FEMA Individual Assistance programs can provide:

- Temporary housing assistance and rental payments

- Home repair grants for damage not covered by insurance (typically capped at amounts far below full repair costs)

- Personal property replacement assistance

- Disaster unemployment assistance

- Crisis counseling referrals

Critical limitations of FEMA assistance:

- FEMA is not allowed to duplicate insurance benefits. If your insurance should cover the loss, FEMA will refer you to your insurer first.

- FEMA will automatically refer applicants to the U.S. Small Business Administration (SBA) for low-interest disaster loans if they meet income thresholds. You must complete and return the SBA loan application to remain eligible for certain FEMA assistance.

- FEMA grant amounts are typically far lower than actual repair or replacement costs.

- Application deadlines are strict — typically 60 days from the disaster declaration date, though late applications may be considered.

For the September 2024 Hurricane Helene emergency declaration (FEMA-3618-EM), FEMA designated Houston County for emergency protective measures under the Public Assistance program. Residents in designated counties could apply through DisasterAssistance.gov or by calling 1-800-621-3362.

The key takeaway: FEMA helps with immediate survival and basic needs, but it does not make you whole. Your insurance policy — and if necessary, a bad faith lawsuit — is the path to full financial recovery.

When a Natural Disaster Causes Injuries or Wrongful Death

Disaster claims are not limited to property damage. When tornadoes, hurricanes, or floods cause physical injuries or death, additional legal claims may be available.

Alabama’s wrongful death statute allows surviving family members to file a lawsuit when a death is caused by “the wrongful act, omission, or negligence of another person.” In the disaster context, this can include:

- Negligent construction — Buildings, mobile homes, or commercial structures that collapse during storms due to code violations or defective construction

- Failure to warn — Employers, event organizers, or property managers who fail to provide adequate shelter or warning

- Utility negligence — Downed power lines, gas leaks, or other infrastructure failures that injure or kill people during or after storms

- Defective products — Generator malfunctions, faulty emergency equipment, or other product failures during disaster response

Disaster-related injuries can also give rise to claims for emotional distress, particularly when an insurance company’s bad faith denial of a property claim compounds the psychological trauma of losing a home.

Alabama’s contributory negligence rule applies to personal injury claims arising from disasters just as it applies to auto accidents. If the defendant can show you were even 1% at fault, your claim may be barred — which makes preserving evidence and avoiding statements that imply fault critical from the very beginning.

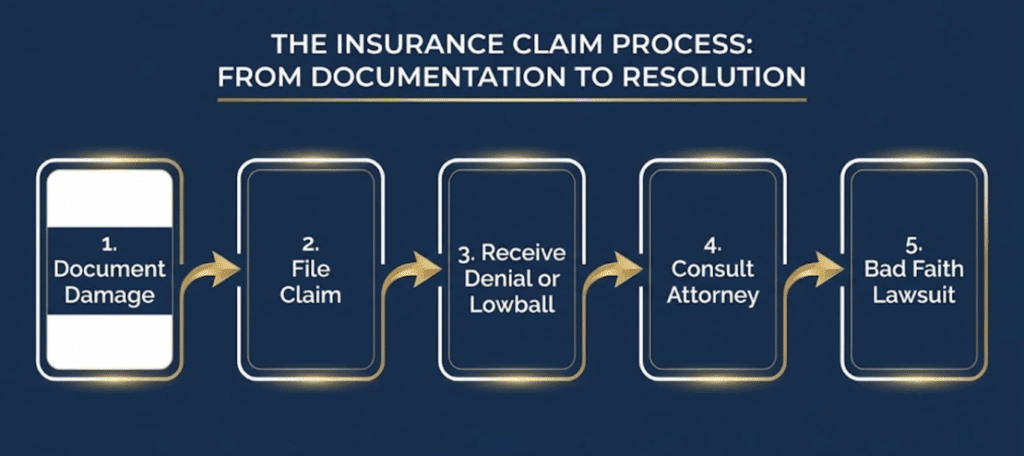

What to Do After a Natural Disaster in Alabama: A Step-by-Step Guide

Based on the documented patterns in Alabama disaster claims litigation and insurance regulations, here are the steps that protect your rights:

Step 1: Ensure safety first. Do not re-enter damaged structures until they have been inspected. Watch for downed power lines, gas leaks, contaminated water, and structural instability.

Step 2: Document everything before cleanup begins. Photograph and video every room, every wall, every piece of damaged property. Capture exterior damage from multiple angles. Document the date and time. This evidence is irreplaceable — once repairs begin or debris is cleared, your proof disappears.

Step 3: File your insurance claim immediately. Contact your insurance company as soon as possible. Alabama Insurance Code Chapter 482-1-125 sets the clock running once you submit proof of loss. The insurer must acknowledge your claim within 15 days and make a decision within 30 days.

Step 4: Apply for FEMA assistance if a disaster has been declared. Visit DisasterAssistance.gov or call 1-800-621-3362. Do this even if you have insurance — FEMA can provide interim assistance while your insurance claim is being processed.

Step 5: Get your own repair estimates. Do not rely solely on the insurance company’s adjuster. Hire an independent contractor or public adjuster to assess your damage. Insurance company adjusters work for the insurer, not for you.

Step 6: Do NOT accept the first settlement offer without review. The initial offer from an insurance company after a disaster is almost always lower than the actual cost of repair. Have an attorney or independent adjuster review the offer before signing anything.

Step 7: Watch for bad faith red flags. If your insurer denies your claim without clear justification, fails to investigate adequately, ignores your calls, demands excessive documentation, or offers a settlement far below your documented losses — these may indicate bad faith under Alabama law.

Step 8: Contact an experienced disaster claims attorney. Alabama’s bad faith insurance laws provide powerful remedies, but proving bad faith requires strong evidence and strategic legal action. An attorney can send a spoliation letter to preserve evidence, negotiate directly with the insurer, and file a bad faith lawsuit if necessary.

Strickland Law Group has represented Alabama disaster victims since forming its dedicated disaster claims practice after the 2011 Super Outbreak. The firm’s attorneys have recovered over $1 billion in total settlements and jury verdicts across all practice areas, and founding partner Michael Strickland has personally tried more than 100 cases to verdict. For disaster claims, call 800-874-3528 or 334-269-3230 for a free consultation.

Conclusion

Alabama’s position as one of the most disaster-prone states in the nation — with 116 billion-dollar weather events since 1980, 40+ tornadoes per year, and regular hurricane threats — means that property damage from natural disasters is not a matter of “if” but “when.” When that day comes, the insurance company you have been paying premiums to for years has a legal obligation to honor its commitments promptly and fairly.

If they fail to do so, Alabama law provides real consequences: bad faith lawsuits that can recover compensatory damages, mental anguish damages, and punitive damages up to three times your compensatory award. You do not have to accept a denied claim or a lowball settlement.

Your first step: document everything. Your second step: call Strickland Law Group at 334-269-3230 or 800-874-3528 for a free review of your disaster claim. The consultation costs nothing, and you pay no fees unless we recover compensation for you.

FAQ

Q: Does standard Alabama homeowners insurance cover tornado damage?

A: Yes. Standard homeowners policies in Alabama cover wind damage from tornadoes, including structural damage, roof damage, and personal property destruction. However, insurers may dispute claims by attributing damage to pre-existing conditions or wear and tear.

Q: Does Alabama homeowners insurance cover flood damage?

A: No. Standard policies exclude flood damage. You need a separate National Flood Insurance Program (NFIP) policy or a private flood insurance policy. Alabama receives an average of 56 inches of rainfall annually, making flood coverage essential for many homeowners.

Q: How long does an Alabama insurer have to respond to my storm damage claim?

A: Under Alabama Insurance Code Chapter 482-1-125, insurers must acknowledge claims within 15 days and accept or deny them within 30 days of receiving proof of loss. Unreasonable delays may constitute bad faith.

Q: What is insurance bad faith in Alabama, and how much can I recover?

A: Bad faith occurs when an insurer denies or underpays a valid claim without legitimate justification. Alabama law allows compensatory damages, mental anguish damages, and punitive damages up to three times compensatory damages (capped at $1.5 million) in proven bad faith cases.

Q: How long do I have to file a bad faith insurance lawsuit in Alabama?

A: The statute of limitations is two years from the date of the insurer’s wrongful action under Alabama Code § 6-2-38. Missing this deadline permanently bars your claim, regardless of how clearly the insurer acted in bad faith.

SOCIAL MEDIA COPY

- 116 billion-dollar disasters have hit Alabama since 1980. If your insurer denied your storm claim, Alabama law fights back. (120 chars)

- Did you know standard Alabama homeowners insurance doesn’t cover floods? Here’s what IS covered — and what to do when it’s denied. (131 chars)

- Alabama bad faith law lets you recover up to 3x damages when insurers wrongfully deny storm claims. Know your rights. (119 chars)

This article references publicly available information from NOAA’s National Centers for Environmental Information (NCEI), the National Weather Service (NWS) Birmingham, the Federal Emergency Management Agency (FEMA), the Alabama Emergency Management Agency, the Alabama Supreme Court, the American Journal of Public Health, and Strickland Law Group, including official disaster data, Alabama Code provisions, court decisions, and published legal analyses dated 1981–2026. All statistics and legal principles described reflect Alabama law as of February 2026. Results in disaster claims cases depend on specific facts, evidence, policy terms, and applicable law. This article is for informational purposes only and does not constitute legal advice. For guidance on your specific situation, contact Strickland Law Group at 334-269-3230 for a free consultation.