A 2024 study published in the Journal of Safety Research by the University of Illinois Chicago found that one-third of rideshare drivers have been involved in a crash while working. When Alabama legalized ridesharing statewide in 2018 under Ala. Code § 32-7C-1, it opened the door to convenient transportation but also created a complex insurance landscape that confuses many accident victims. The difference between understanding which “period” applies to your accident can mean the difference between accessing $25,000 in coverage or $1 million. This guide explains exactly how these three insurance periods work under Alabama law and what you need to do to protect your right to compensation.

What Are Rideshare Insurance Periods? Understanding the System Through Real Coverage Requirements

When the Alabama legislature approved ridesharing in 2018, it established specific insurance requirements for Transportation Network Companies (TNCs) like Uber and Lyft under Ala. Code § 32-7C-2. Unlike traditional taxi services that maintain continuous commercial insurance, rideshare companies shift coverage responsibility based on what the driver is doing at the exact moment of a crash.

According to Uber’s official insurance documentation published in August 2024, this creates three distinct “periods” that determine which insurance policy responds to an accident. The Alabama Code specifically mandates different minimum coverage amounts for each period, directly affecting how much compensation is available to injured passengers, other motorists, pedestrians, and cyclists.

This period-based system exists because rideshare drivers use their personal vehicles and toggle between personal use and commercial activity throughout their shifts. Understanding which period applies to your accident is the first critical step in any Alabama rideshare injury claim.

Period 1: App On, Waiting for a Ride Request

What Happens During This Period

Period 1 begins when a rideshare driver opens the Uber or Lyft app and makes themselves available to accept ride requests. The driver is logged into the network but has not yet been matched with a passenger. During this time, they may be driving around, parked, or traveling to a location where they expect ride requests.

Coverage Available Under Alabama Law

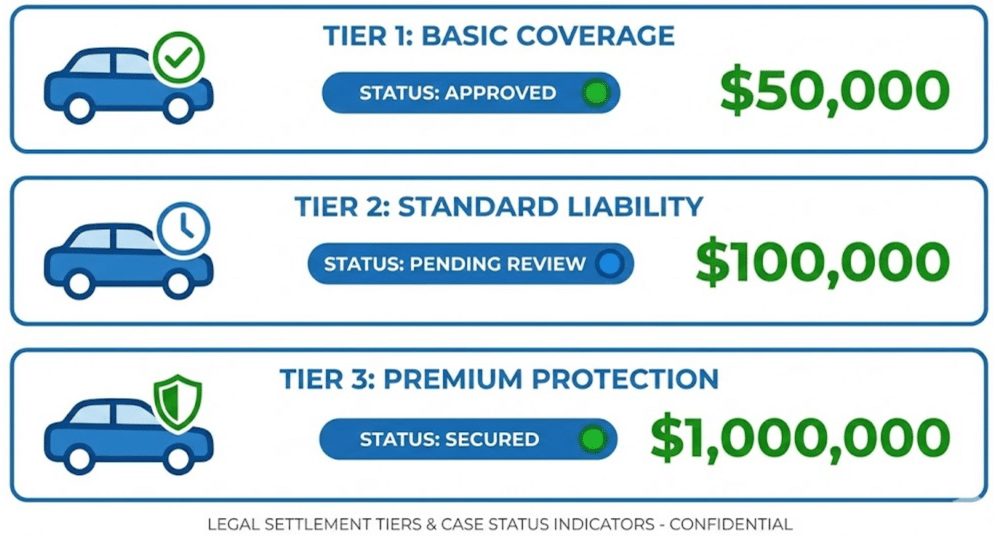

Alabama Code § 32-7C-2 requires TNCs to maintain the following minimum coverage during Period 1:

- $50,000 per person for bodily injury

- $100,000 per accident for bodily injury (when multiple people are injured)

- $25,000 for property damage

This coverage is contingent, meaning it only activates if the driver’s personal auto insurance denies the claim or provides insufficient coverage. Most personal auto policies exclude commercial activity, creating a coverage gap that the TNC policy is designed to fill.

Why Period 1 Creates the Greatest Risk

According to insurance industry analysis, Period 1 represents the most dangerous coverage gap for accident victims. The $50,000/$100,000 limits may sound substantial, but severe injuries routinely exceed these amounts. A single hospitalization for trauma can generate medical bills exceeding $100,000, leaving victims with uncovered expenses.

Neither Uber nor Lyft provides collision or comprehensive coverage during Period 1. If the rideshare driver’s vehicle is damaged, they must rely on their personal policy, which may deny the claim due to commercial use exclusions.

Period 2: Ride Accepted, En Route to Pickup

What Happens During This Period

Period 2 begins the moment a driver accepts a ride request and starts traveling to pick up the passenger. The driver is now engaged in a prearranged ride under Alabama law, triggering significantly higher coverage requirements.

Coverage Available Under Alabama Law

Under Ala. Code § 32-7C-2, once a driver is engaged in a prearranged ride, TNCs must provide primary automobile liability insurance of at least $1 million for death, bodily injury, and property damage combined.

Both Uber and Lyft’s official documentation confirms this coverage includes:

- $1 million in third-party liability coverage

- Uninsured/underinsured motorist coverage

- Contingent comprehensive and collision coverage (if the driver maintains such coverage on their personal policy), subject to a $2,500 deductible

The Practical Impact of Period 2 Coverage

The jump from $100,000 in Period 1 to $1 million in Period 2 represents a tenfold increase in available coverage. For victims with catastrophic injuries, this difference fundamentally changes the viability of obtaining full compensation.

However, the contingent nature of collision coverage creates complications. If a rideshare driver does not carry comprehensive and collision on their personal policy, neither Uber nor Lyft provides this coverage. The driver’s vehicle damage remains their responsibility, which can affect their willingness to cooperate with accident investigations.

Period 3: Passenger in the Vehicle

What Happens During This Period

Period 3 covers the time from when a passenger enters the rideshare vehicle until they exit at their destination. This is when rideshare companies provide their maximum coverage.

Coverage Available Under Alabama Law

The same $1 million coverage requirement from Period 2 continues throughout Period 3. Under both Uber and Lyft’s policies, passengers in the vehicle during Period 3 have access to:

- $1 million in liability coverage for injuries caused by the rideshare driver

- $1 million in uninsured/underinsured motorist coverage if another at-fault driver lacks adequate insurance

- Contingent comprehensive and collision coverage with a $2,500 deductible

Alabama’s Guest Statute Exception for Rideshare Passengers

Alabama maintains one of the few remaining guest statutes in the country under Ala. Code § 32-1-2. This law generally prevents passengers from suing drivers who gave them a free ride unless the driver engaged in willful or wanton misconduct.

However, rideshare passengers are explicitly exempt from this limitation. Because Uber and Lyft passengers pay for their rides, they are not considered “guests” under Alabama law. This distinction, confirmed by Alabama courts, means rideshare passengers can pursue compensation for injuries caused by their driver’s ordinary negligence, not just reckless behavior.

How Alabama’s Fault-Based System Affects Your Rideshare Claim

Alabama operates under a fault-based insurance system, meaning the person or party responsible for causing an accident bears financial responsibility for the resulting damages. This applies to rideshare accidents just as it does to any other motor vehicle collision.

Alabama’s Contributory Negligence Rule

Alabama is one of only four states that follows pure contributory negligence. Under this doctrine, if you bear any fault for the accident, even 1%, you may be completely barred from recovering compensation. This makes evidence preservation and accurate accident reconstruction critical in rideshare cases.

For example, if an investigation reveals that a passenger distracted the rideshare driver immediately before a crash, the defense may argue the passenger contributed to the accident. An experienced attorney can anticipate and counter such arguments.

Statute of Limitations

Under Alabama law, you have two years from the date of a rideshare accident to file a personal injury lawsuit. Minors have until two years after their 19th birthday. Missing this deadline typically eliminates your right to pursue compensation through the courts, regardless of how strong your case may be.

Determining Liability in Alabama Rideshare Accidents

Multiple Potentially Liable Parties

Rideshare accidents often involve more liability complexity than standard car crashes. Depending on the circumstances, the following parties may share responsibility:

The rideshare driver may be liable if their negligence, such as distracted driving, speeding, or violating traffic laws, caused or contributed to the collision. Alabama law holds all motorists to a duty of reasonable care.

The rideshare company itself may bear some responsibility under certain circumstances, particularly if inadequate driver screening, training deficiencies, or policy failures contributed to the accident.

Other motorists may be fully or partially at fault if their actions caused the crash. In such cases, victims may pursue claims against that driver’s insurance while the rideshare company’s uninsured/underinsured motorist coverage provides backup protection.

Vehicle or parts manufacturers could be liable if a defect contributed to the crash, converting the case into a product liability matter.

Why the Driver’s App Status Is Critical Evidence

Insurance adjusters and attorneys focus intensely on determining the exact app status at the moment of impact. The difference between Period 1 and Period 2 represents a potential $900,000 difference in available coverage.

Evidence that can establish app status includes:

- The rideshare company’s electronic records showing when rides were accepted and completed

- GPS data from the driver’s phone

- The passenger’s app records showing ride request and acceptance times

- Witness statements about whether a passenger was present in the vehicle

What to Do After an Alabama Rideshare Accident

Immediate Steps at the Scene

Seek medical attention for any injuries. Even if you feel fine, some injuries do not present symptoms immediately. Medical documentation from the day of the accident creates important evidence linking your injuries to the collision.

Contact law enforcement to file an accident report. Alabama law requires reporting accidents involving injury, death, or property damage exceeding $250. The police report provides an official record of the accident circumstances.

Document everything possible. Photograph vehicle damage, the accident scene, traffic signals, weather conditions, and any visible injuries. Obtain contact information from witnesses.

Note the rideshare driver’s information, including their name, license plate, and the vehicle make and model displayed in your app.

Reporting to the Rideshare Company

Both Uber and Lyft maintain accident reporting systems. For Uber, you can report through their online accident claim form. Lyft provides a similar online reporting system. Document your submission and retain confirmation.

Be cautious about recorded statements to insurance adjusters before consulting with an attorney. Adjusters may attempt to establish facts that reduce the company’s liability or suggest you contributed to the accident.

Why Legal Representation Matters in Rideshare Cases

Rideshare accident claims involve navigating multiple insurance policies, understanding app-based evidence, and countering defense strategies unique to this industry. Insurance companies representing Uber and Lyft have extensive experience minimizing payouts.

At Strickland Law Group, our attorneys have represented injury victims throughout Alabama since 1994. The firm has secured over $1 billion in settlements and judgments for clients, including significant recoveries in complex auto accident and wrongful death cases. Michael Strickland, the firm’s founding partner, has personally tried more than one hundred cases and understands how to hold negligent parties accountable.

Conclusion

The three insurance periods governing Uber and Lyft accidents in Alabama create a coverage landscape that directly determines how much compensation may be available for your injuries. Period 1 offers limited coverage of $50,000/$100,000, while Periods 2 and 3 provide up to $1 million in protection. Understanding which period applies, preserving evidence of app status, and navigating Alabama’s contributory negligence rules requires experienced legal guidance.

If you or a loved one has been injured in an Alabama rideshare accident, contact Strickland Law Group for a free consultation. Our team can analyze your case, identify all available insurance coverage, and pursue the maximum compensation you deserve. Call 334-269-3230 today.

Frequently Asked Questions

What insurance coverage applies if an Uber driver hits me while I’m walking in Alabama?

If the driver had the app on, you can access the TNC coverage for that period. During Periods 2 and 3, this means up to $1 million in liability coverage. During Period 1, coverage is limited to $50,000 per person.

Can I sue Uber or Lyft directly for my Alabama accident injuries?

Generally, rideshare companies structure their driver relationships as independent contractors, limiting direct liability. However, claims may be possible if company policies or screening failures contributed to the accident. An attorney can evaluate your specific circumstances.

How long do I have to file a rideshare accident lawsuit in Alabama?

Alabama’s statute of limitations gives you two years from the accident date to file a personal injury lawsuit. Minors have until two years after turning 19.

What if the rideshare driver’s personal insurance denies my claim?

TNC coverage under Alabama law is designed to fill this gap. If the driver’s personal policy excludes commercial activity, Uber or Lyft’s contingent coverage should apply based on the driver’s app status.

Does Alabama’s guest passenger law affect my rideshare injury claim?

No. Because rideshare passengers pay for their rides, they are not considered guests under Ala. Code § 32-1-2. You can pursue claims based on ordinary negligence, not just willful misconduct.